Introduction

Increasingly, organisations are voluntarily accounting for the social, governance and environmental aspects of their operations. This accountability is not only important for shareholders and financial institutions. Consumers, employees, trade unions, local residents and other stakeholders also demand transparency and consistent reporting on the governance, social and environmental aspects of the organisation. In English, these are called Environmental, Social and Governance (ESG) aspects. The Global Reporting Initiative (GRI) was one of the first organisations to develop guidelines for sustainability reporting.

Global Reporting Initiative

The Global Reporting Initiative was founded in 1997 in Boston, USA, and published the first version of the then GRI standard (G1) in 2000. This standard provided the first global standard for sustainability reporting.

GRI is now the global standard for sustainability reporting and is used by leading institutional investors, government agencies, corporations and development organisations around the world. The standards provide organisations with guidelines and reporting tools to report on economic, social and environmental performance.

What is a standard?

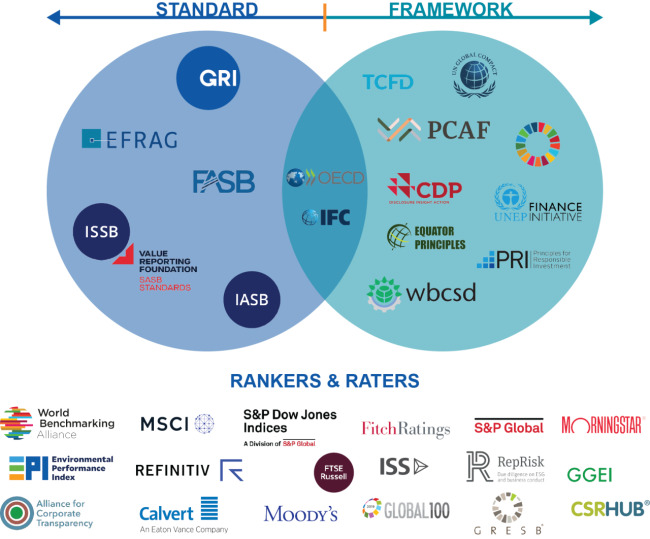

Sustainability reporting is usually based on standards and frameworks, both providing guidance on how companies report on sustainability. A standard contains a detailed reporting structure with strict ESG criteria that companies must report on. Because the reporting requirements are defined, the results are (annually) reproducible and consistent (and therefore comparable).

A framework is less specific; it contains more the principles, which topics should be covered and how to report on these topics. Frameworks are used by companies on a voluntary basis and usually do not contain specific criteria and metrics.

Standards and frameworks are not mutually exclusive, but rather complementary (see diagram below, source GRI).

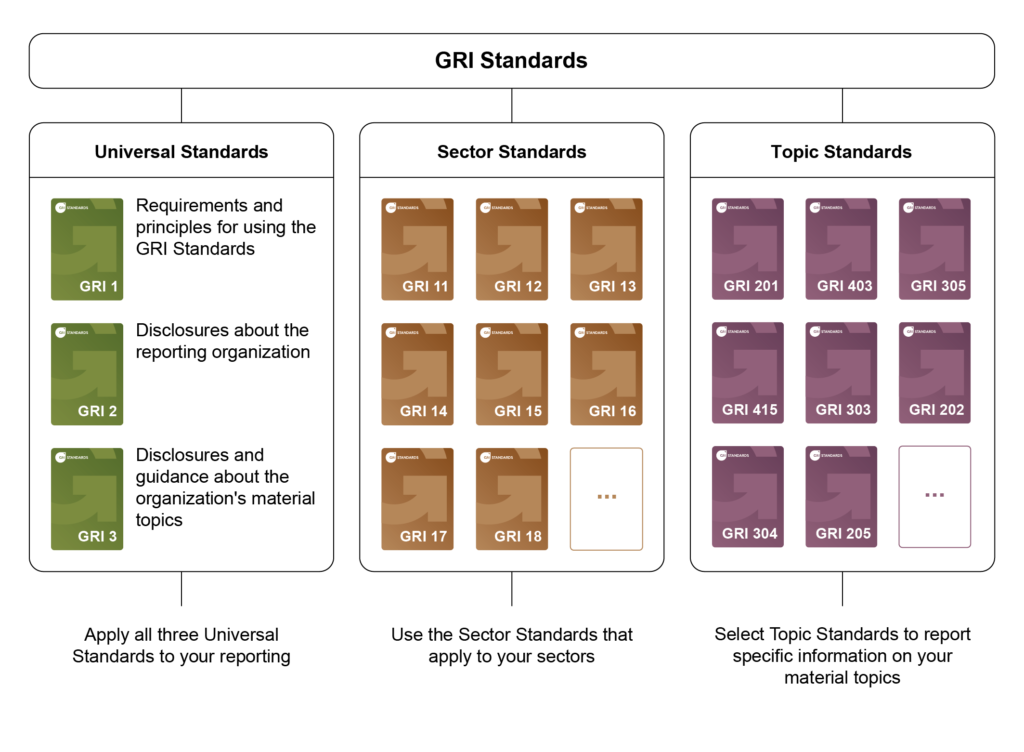

Structure of GRI standards

The GRI standards are modular and consist of three sets of standards:

- The GRI Universal standards describe, among other things, the purpose of the standards and how to report. The universal standards apply to all organisations.

- De GRI Sector standaarden are available for oil & gas, mining, aquaculture and fisheries. Work is currently underway on 37 other sector standards to be released in the coming years.

- The GRI Topic Standards describe specific topics, e.g. waste, health & safety, taxes. The Subject Standards are divided into three subcategories: governance (GRI 200), environment (GRI 300) and social (GRI 400).

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

Each standard begins with a detailed explanation of its use. The standards contain explanations that provide a structured way for an organisation to report information about itself and its impact.

How to get started with the GRI framework

Universal standards: mandatory for every organisation

- GRI 1 describes the requirements and principles of the GRI standards

- GRI 2 describes the reporting organisation (size, structure, context, shareholders, etc.)

- GRI 3: describes the determination ofmaterial threads

Material threads are governance, environmental, and social issues that have material impact on the organisation’s environment. Impact can be positive or negative, actual or potential, direct or indirect, short- or long-term and intended or unintended. Material threads are drawn up on the basis of amateriality assessment.

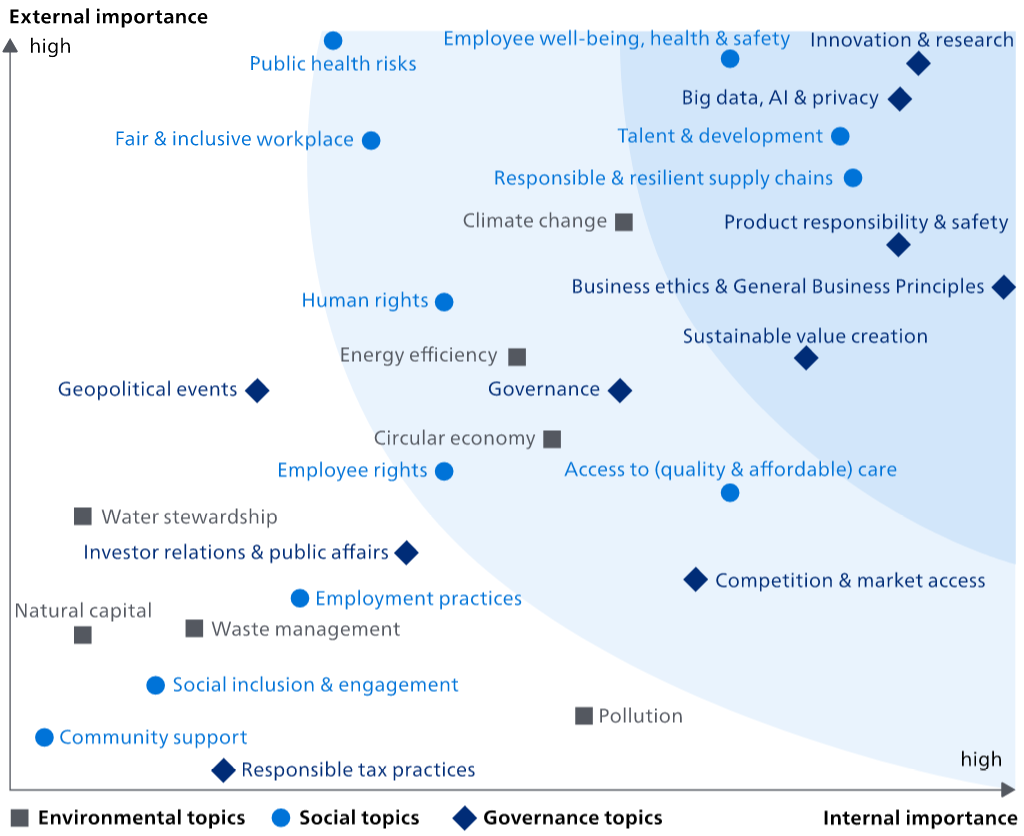

If the list ofmaterial threads has been established, eachtopic determined the importance of the impact, then for the most weightythreads established how this will be reported. See below an example from Royal Philips of their materiality assessment matrix.

- Sector standards: only applicable for relevant sectors

Sector standards contain the most likelymaterial threads for the relevant sector. Currently, standards are available for 4 sectors: oil & gas, mining, aquaculture and fisheries. - Topic standards: information on a broad spectrum of topics on which organisations can report. De topic standaarden moeten aansluiten bij de material topics as determined by the organisation. Examples of topic standards are child labour, diversity, biodiversity, health & safety and privacy.

- Stakeholder engagement

Based on themateriality assessment can be identified which stakeholders in influenced by the reporting organisation or which stakeholders may have a decisive influence on the reporting organisation. The reporting organisation should identify its stakeholders and explain how it has responded to their expectations and interests. - Data collection and reporting

GRI prescribes what and what an organisation should do for eachmaterial topic must report, however, the manner in which is not prescribed. An organisation can therefore decide for itself whether it uses ESG reporting software and, if so, which package. - Compile and publish GRI table of contents Sustainability reports based on the GRI standards must include a table of contents so that specific information can be easily found. Should an organisation not report on parts of a standard, the reason should be specified in the table of contents. The reporting process is concluded by publishing the sustainability reports and submitting the table of contents to GRI.

Key benefits of (sustainability) reporting

- Transparent and open: a company can share its rating with others without releasing commercially sensitive information.

- Standardised approach: the GRI indicators, guidelines and reporting requirements provide a framework within which public and private organisations can report on their sustainability performance.

- Gap analysis: GRI allows organisations to compare their own performance and risks with other companies and identify improvements.

- Engagement: the reports allow the company to communicate with stakeholders about its sustainability performance by using the same information and reporting framework.

- Co-creation: GRI is a jointly developed initiative and not owned by any organization. It represents the consensus of investors and other stakeholders on what information is most important for understanding an organization’s impact on society and the environment, who should report it, and how it should be reported.

Goal 17 and GRI

Within Goal 17, several consultants are GRI certified. They have knowledge and experience in establishing a materiality matrix, preparing and setting up GRI sustainability reports and setting up supporting collection and reporting software.

If you are considering becoming GRI compliant and need help in doing so, please contact us atinfo@goal17.eco.